Online Store

Online Store

Introduction

Over the last several decades, governments have collectively pledged to slow global warming. But despite intensified diplomacy, the world is already facing the consequences of climate…

Renewing America Progress Report: Federal Debt and Deficits

More on:

It’s not often that one hears the phrase “European steeliness.” But while the United States continues to punt its serious tax and spending problems ever farther down the field, Europe’s big economies have actually done something about fiscal challenges that were even bigger than those facing the United States.

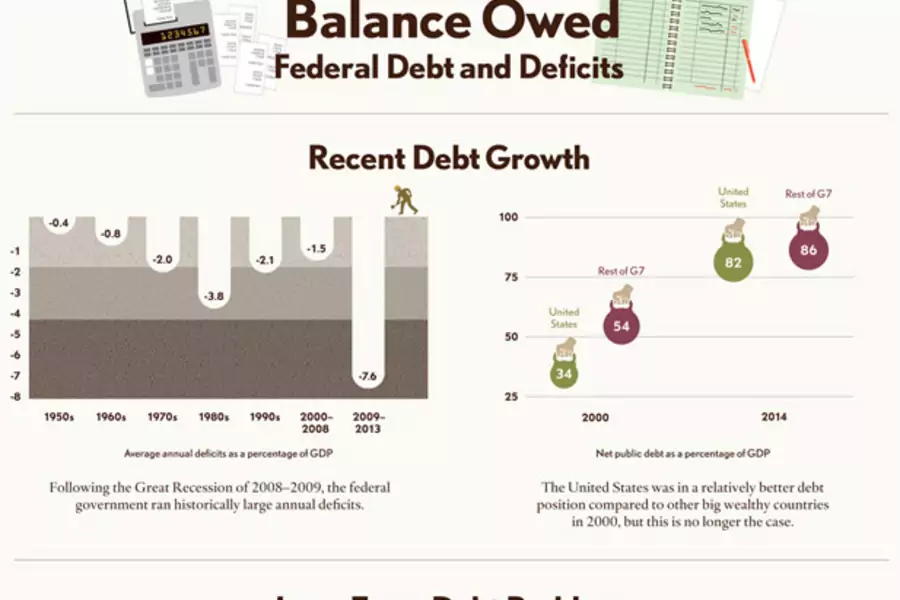

That is the conclusion of the new Renewing America Progress Report and Scorecard, “Balanced Owed: Federal Debt and Deficits,” by my colleague Rebecca Strauss, who also authored a companion piece that appeared today in Quartz. America’s politicians claim to be deeply worried about the growing federal debt. Fights over federal spending have roiled Congress, and in part led to last year’s government shutdown. But our lawmakers have done little to actually bring America’s federal balance sheet in line.

In the short term, a somewhat stronger economy, the slowing growth of health care costs and the deep cuts to federal discretionary spending as a result of sequestration have all helped to reduce the huge deficits run during the Great Recession. But in the longer term, as America’s population ages and spending on Social Security and health care rise, the picture remains as bleak as ever. If current trends continue, the costs are clearly unsustainable. By 2040, U.S. government debt will total, by the most conservative estimates, more than 110 percent of GDP (compared with just 34 percent in the year 2000); nearly four out of every five federal dollars will be spent on entitlement programs and interest payments.

Europe faces the same budgetary problems, and without some of the U.S. advantages. The American population is younger, our old people are wealthier and rely less on public spending during their retirement. U.S. taxes are also much lower. Yet despite these advantages, the failure of the U.S. government to respond has actually left the United States in a worse position than the major countries of Europe. France, Germany and Italy have each taken politically difficult steps to reduce spending on the elderly, tying future benefit increases either to inflation, tax revenues or life expectancy. That means that, compared with the previous spending trajectory, public pensions costs by 2040 will fall 30 percent in France, 40 percent in Germany, and almost 50 percent in Italy.

In contrast the United States has done……. well, almost nothing. Washington has cut about 10 percent from the small portion of “discretionary” federal spending such as defense, education, infrastructure etc., leaving the country less able to defend itself in an increasingly unstable world, less educated at a time when education is the key to advancement, and left to watch its roads and bridges crumble and its water pipes explode. But it has done little either to raise revenue or to reduce the costs of the big entitlement programs that drive the federal deficit. And the longer we wait, the higher proportion of federal spending will go simply to paying off past debts.

The American failure is, in good measure, due to a notable lack of “steeliness” on the part of the political class in Washington. Bringing federal debt under control requires unpopular decisions. There is a limited set of choices: raise taxes, cut entitlements such as Social Security and Medicare, or further slash federal spending on discretionary programs. Realistically some of all three is probably necessary. But Americans want neither spending cuts nor tax increases, and both Democrats and Republicans have pandered to one side of that preference, making any “grand bargains” – or even little bargains – impossible.

Will it embarrass our politicians to learn that the supposedly weak-willed European leaders have shown far more resolve? Probably not. But it certainly should.

More on: